Home care agency profitability concerns jumped from 13% to 34% in a single year as the U.S. home-based care market reached $173.6 billion in 2026, according to industry survey data published by myEZcare on June 2. The sharp rise in financial pressure reflects simultaneous strain from rising caregiver wages, tighter Medicaid reimbursement, and administrative compliance overhead, even as the market grew 4.1% year-over-year.

TL;DR: Home care profitability concerns tripled from 13% to 34% in 2026 as the $173.6 billion U.S. market faces a projected 25% workforce shortfall by 2030, with 61% of providers citing client affordability and rising costs as extreme growth obstacles.

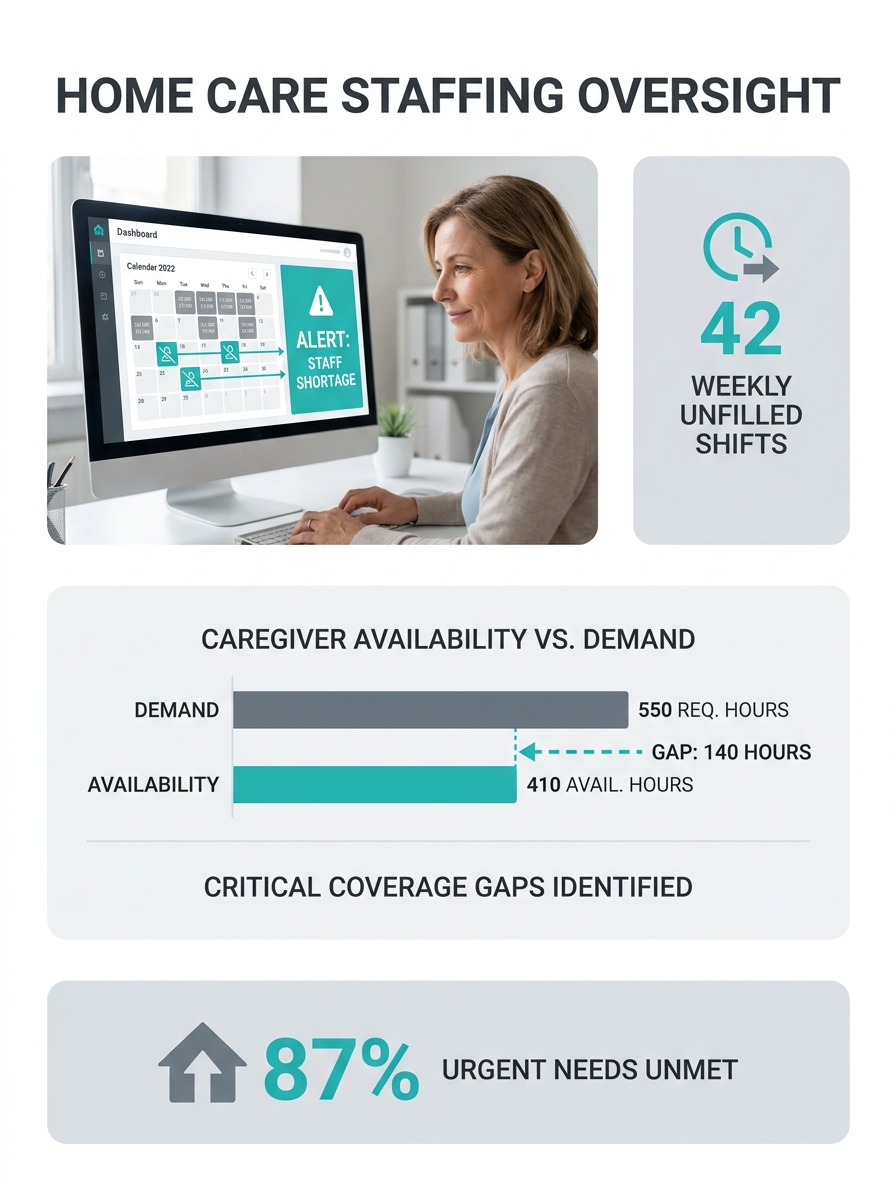

The AxisCare 2026 Home Care Industry Survey documented the shift in what agency leaders identify as top operational pain points. Caregiver shortages remain the most pressing concern at 53% of respondents, down slightly from 59% the prior year. But for the third consecutive year, client affordability and rising costs of staff, supplies, and services remain the most significant obstacles to growth, with 61% of industry leaders rating these challenges as very big or extreme hindrances, according to the report.

Market Growth Outpaces Workforce Pipeline

The global home healthcare market reached approximately $458 billion in 2026 and is projected to grow at a compound annual rate of 10.5% through 2033, according to Grand View Research data cited in the report. North America accounts for roughly 42% of global market share, driven by demographic forces that show no sign of slowing.

Approximately 10,000 Baby Boomers turn 65 every day in the United States, a rate that continues through the end of this decade. By 2030, roughly 20% of the U.S. population will be of retirement age. The preference data compounds demand pressure: 88% of seniors prefer to age in their own homes rather than in a care facility.

The U.S. Bureau of Labor Statistics projects a 22% growth in employment of home health and personal care aides from 2022 to 2032, among the fastest of any occupation in the U.S. economy. But the BLS also estimates a potential 25% shortfall in home health workers by 2030 unless structural changes in training, compensation, and workforce development are made.

The disconnect between demand growth and workforce supply creates what the report characterizes as “constraint that doesn’t limit capacity equally”, agencies with more efficient operational infrastructure can absorb volume that overwhelms competitors still managing disconnected systems. The workforce pipeline gap makes caregiver retention strategies built around reducing job friction, rather than only increasing compensation, a differentiating competitive factor.

Reimbursement and Compliance Pressure

The profitability squeeze documented in the survey reflects multiple simultaneous pressures. Medicaid reimbursement rates, which fund a significant portion of home-based care, have not kept pace with wage increases required to attract and retain caregivers in a tight labor market. Electronic visit verification (EVV) compliance overhead adds administrative cost without generating revenue. Payer requirements have grown more complex, increasing billing coordination costs.

The report notes that rising caregiver wages, necessary to compete for scarce labor, create margin pressure that agencies cannot fully pass through to clients already constrained by affordability concerns. Sixty-one percent of providers cite this cost-affordability tension as a very big or extreme hindrance to growth.

States have begun exploring skill-based Medicaid rate structures that differentiate reimbursement based on caregiver qualifications, a model shift that could eventually reshape agency economics but adds near-term complexity.

Technology and Operational Infrastructure

The report identifies home care software platforms that integrate electronic visit verification, scheduling, documentation, and billing in a single system as infrastructure investments that reduce the coordination cost of managing multiple disconnected tools. Agencies managing paper-based processes face documented overhead costs, with prior research quantifying paper-based agency administrative burden at 11 hours weekly per coordinator.

The operational efficiency gap matters more in a constrained environment. Agencies that can handle higher client volume per coordinator and reduce administrative friction in caregiver workflows gain capacity advantages that translate directly to market share in regions where workforce availability limits everyone’s growth ceiling.

The survey data suggests agencies gaining competitive ground in 2026 are not necessarily the largest or best-funded, but those whose operational infrastructure handles volume, compliance, and billing efficiently enough that workforce and reimbursement constraints limit their capacity less than competitors.

What This Means for Owners

The profitability pressure documented in the 2026 survey data is not cyclical, it reflects structural misalignment between demand growth, workforce supply, and reimbursement adequacy that will define competitive outcomes over the next five years. Agencies still operating on assumptions from the pre-EVV, pre-shortage environment face margin compression that limits investment in the recruitment, retention, and technology infrastructure required to compete for constrained labor.

The workforce shortfall projected at 25% by 2030 means recruitment alone cannot solve capacity constraints. Retention becomes the higher-use variable, and retention strategies built around reducing caregiver job friction, scheduling predictability, efficient communication, simplified documentation, require operational systems that most fragmented software stacks cannot deliver. The agencies treating technology infrastructure as mission-critical rather than back-office overhead are building for the operating environment the data describes, not the one that existed five years ago.

Client affordability pressure cited by 61% of providers as an extreme growth obstacle limits pricing power even as costs rise. That leaves operational efficiency as the primary available margin lever, which makes the integration density of your home care software platform a financial decision rather than just an IT decision.